Virtual Cards: The Good, The Bad, and The Ugly

By Ernie Humphrey, CTP, Treasury Webinars

There has been quite a bit of hype around virtual cards. As a treasury professional at heart, I have been curious about the actual realm of virtual cards, and that is one reason I partnered with Stampli to conduct the “How & Why Companies Make Payments” survey. The survey garnered responses from 386 companies located in the US, and come from across a diverse set of industries in addition to company sizes. The results offer a few trends and help reveal a lack of transparency that exists among all parties involved in a virtual card transaction. It is time to shed some light.

The Good

A virtual card is a unique 16-digit card number that is created solely for a single-use between a payor and a payee. There can be benefits to virtual cards for the payor and the payee. Payors get rebates from virtual card providers based on the dollar amount on a virtual card, and virtual cards make payment processing more efficient, and are a secure form of payment — meaning they help mitigate payment fraud exposures. Payees acquire predictability for when they are getting paid, and if they receive the remittance information, the payee in turn comes by lower accounts receivable (AR) processing costs. A clear win-win, right? That is what some accounts payable (AP) automation suppliers who offer virtual cards would like customers and prospects to think, but that is not quite that easy.

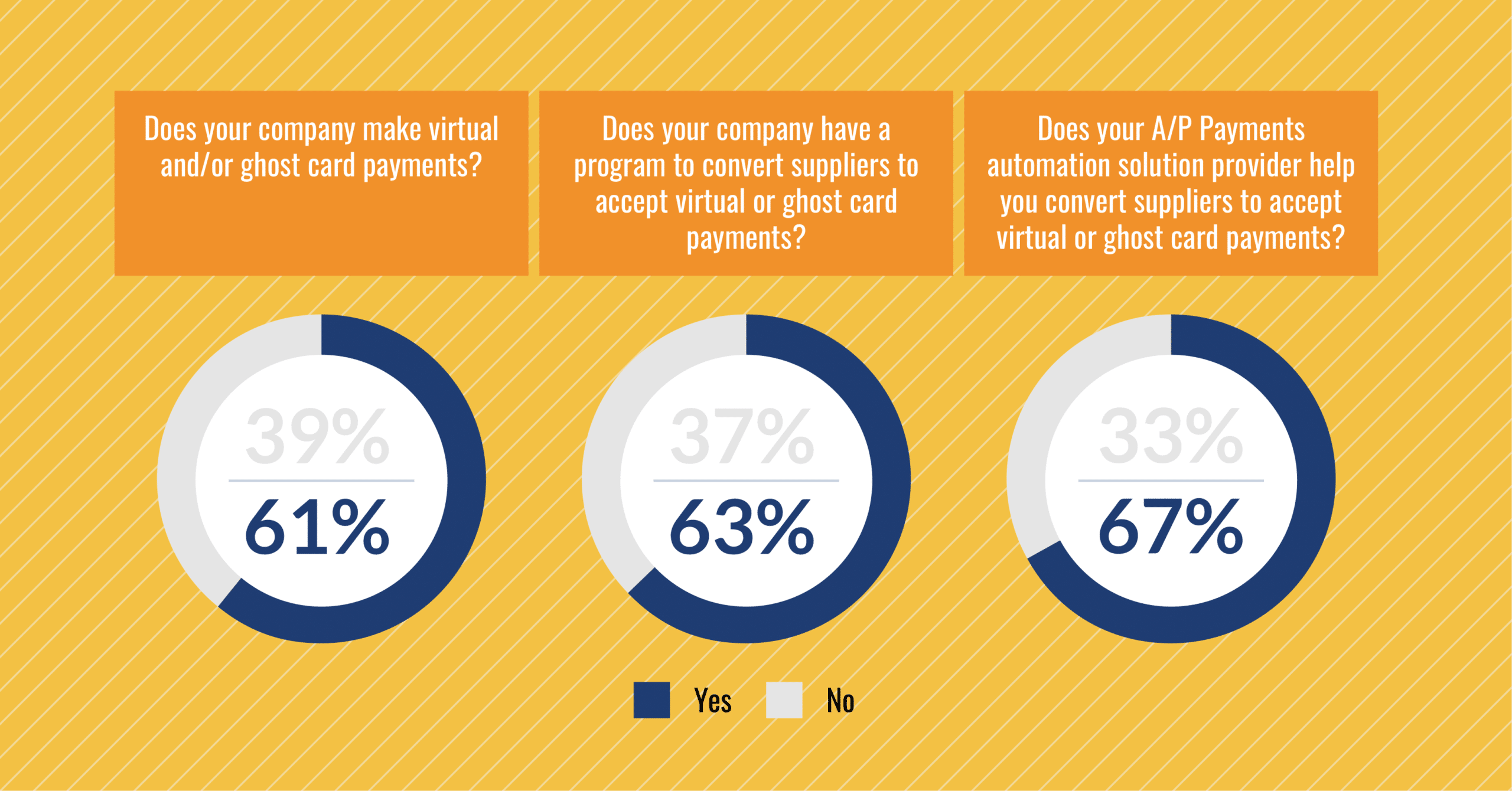

The results of the “How & Why Companies Make Payments” survey suggest that virtual cards are seeing greater adoption and companies are willing to work with AP automation providers to offer programs to pay suppliers via a virtual card as depicted in Figure 1.

The Bad

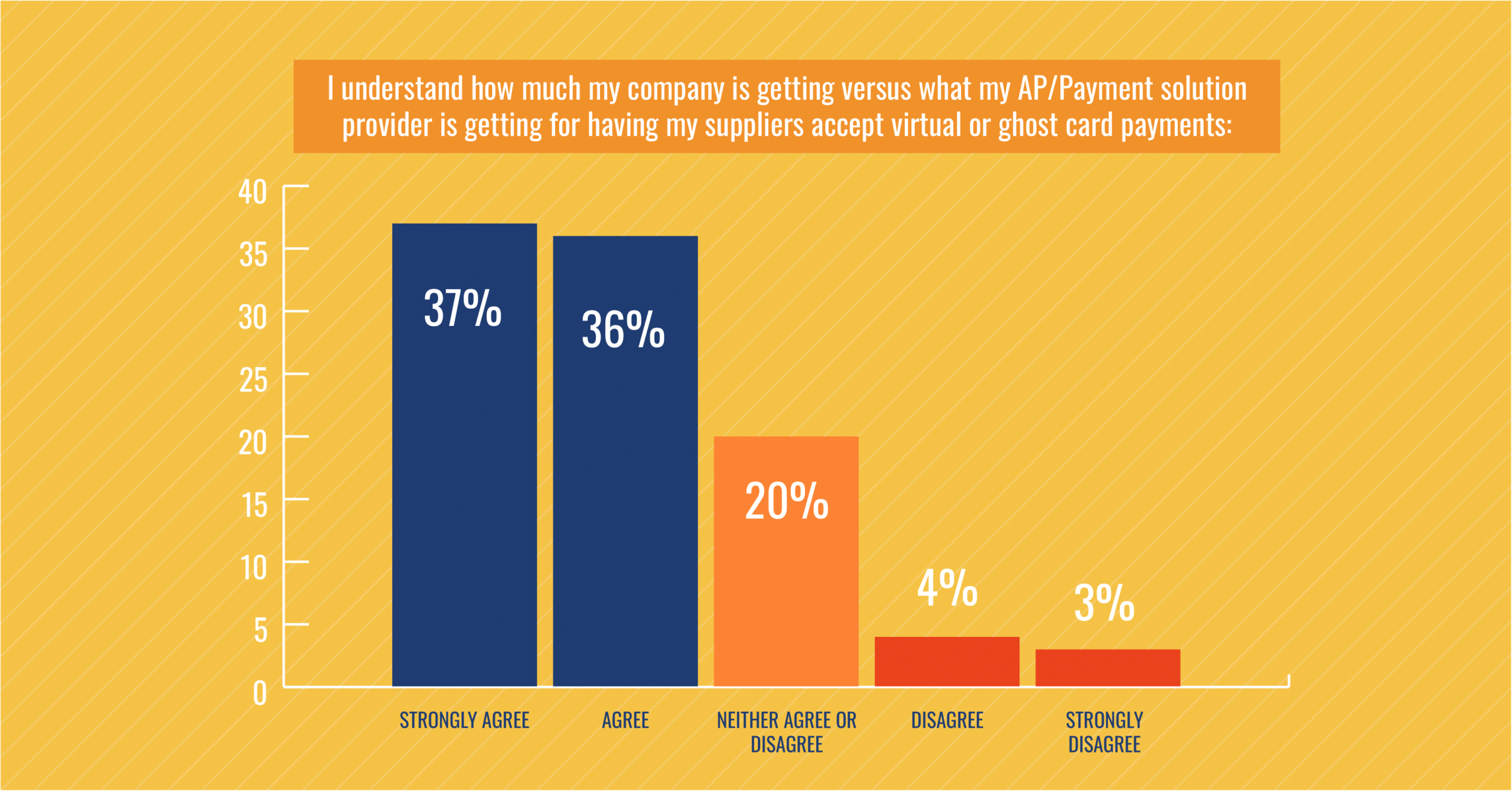

Many companies do not understand what virtual card providers are getting when they push virtual cards on to their suppliers. This conjecture is supported by the aforementioned survey results in Figure 2.

Furthermore, companies report that their suppliers do not understand the accompanying costs in accepting a virtual card payment. To be conservative, we can assume that is 2.5% of the amount of a virtual card transaction. This assertion is supported by the survey results depicted in Figure 3.

The Ugly

Many companies are just not receiving the benefits from programs offered by AP automation solutions providers; to enumerate, the program of convincing their suppliers to accept virtual cards. Supplier relationships matter and companies would do well to protect these relationships and not let an outside party cajole them to take actions that may offer a short-term financial gain while damaging relationships, which can erode a companies competitive advantage.

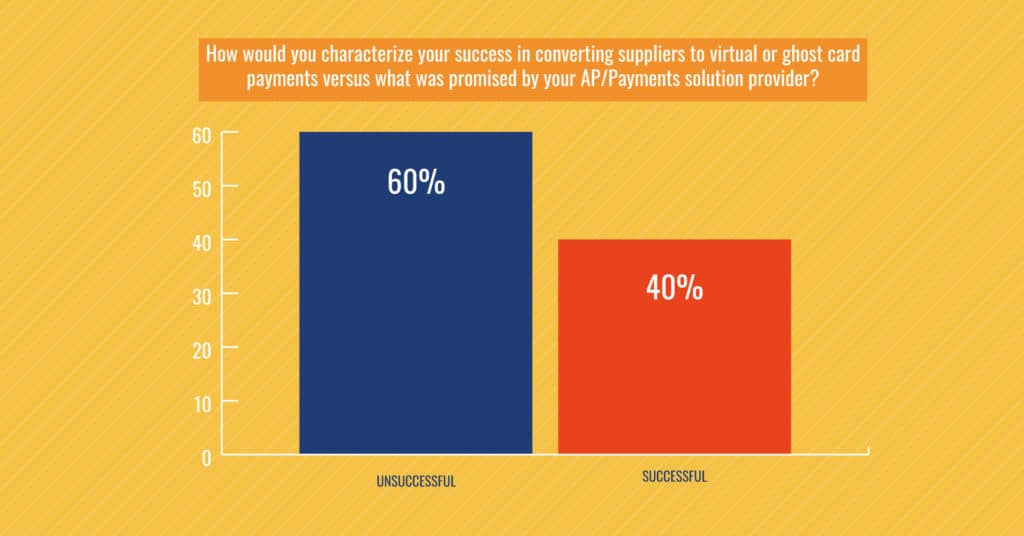

Figure 4 illustrates whether survey respondents found the AP automation solution providers virtual card conversion program successful, or if the promises made from AP automation solution providers were not kept. Sixty percent (60%) of companies that work with AP automation solution providers in such programs conveyed that the conversion programs were unsuccessful and fell short of what was promised to them.

The Bottom Line of Virtual Cards

There are meaningful cost savings and rebates to be had by companies in converting suppliers from being paid by check to being paid via a virtual card. However, the needs to be transparent among payor, payee, and those AP automation providers who facilitate virtual card payments.

Virtual cards are not evil. However, companies should leverage them by working with suppliers to educate them as to the costs and benefits in accepting virtual cards. Companies should not pressure or force suppliers to accept a virtual card payment type because it offers the company (payor) a rebate. Supplier relationships matter and damaging them by forcing/strongly suggesting suppliers be paid on your terms can “inhibit company growth.” Those are words that will make any CFO cringe.

For a comprehensive analysis of the survey report, I invite you to read the How & Why Companies Make Payments whitepaper.