P Card vs. Credit Card: When Virtual Cards are the Way to Go

It’s no secret that credit cards are a popular payment method for businesses.

A 2021 survey report of 361 accounting and finance professionals by Stampli and Treasury Webinars, “How & Why Companies Choose Payment Types” found that 36% of companies preferred using credit cards to pay their suppliers, making it the most-favored payment method, more so than checks, the ACH, and virtual or ghost cards.

Still, just because a payment method might be less popular doesn’t mean it lacks situational advantages for businesses. Today, we’re going to explore when purchase cards, or P cards make sense to use over credit cards and why Stampli Card is a superb payment solution.

Why Some Businesses Shun Credit Cards – And Why P Cards are a Good Alternative

Aside from 36% of businesses preferring to pay suppliers by credit card, here’s another interesting stat: Only 48% of businesses make payments by credit cards. Looked at differently, credit cards are polarizing for the business community. Three-quarters of the companies that use them prefer them. But the majority of businesses look to other payment methods.

In fact, the most frequent form of B2B payment is the “much-maligned” but nonetheless resilient paper check, used by 81% of companies, according to PYMNTS research. The second most frequent B2B payment method is the automated clearing house, or ACH, which is used by 64% of firms. The ACH has rapidly gained in popularity during the COVID-19 pandemic, with payments through it increasing 33.2% in two years.

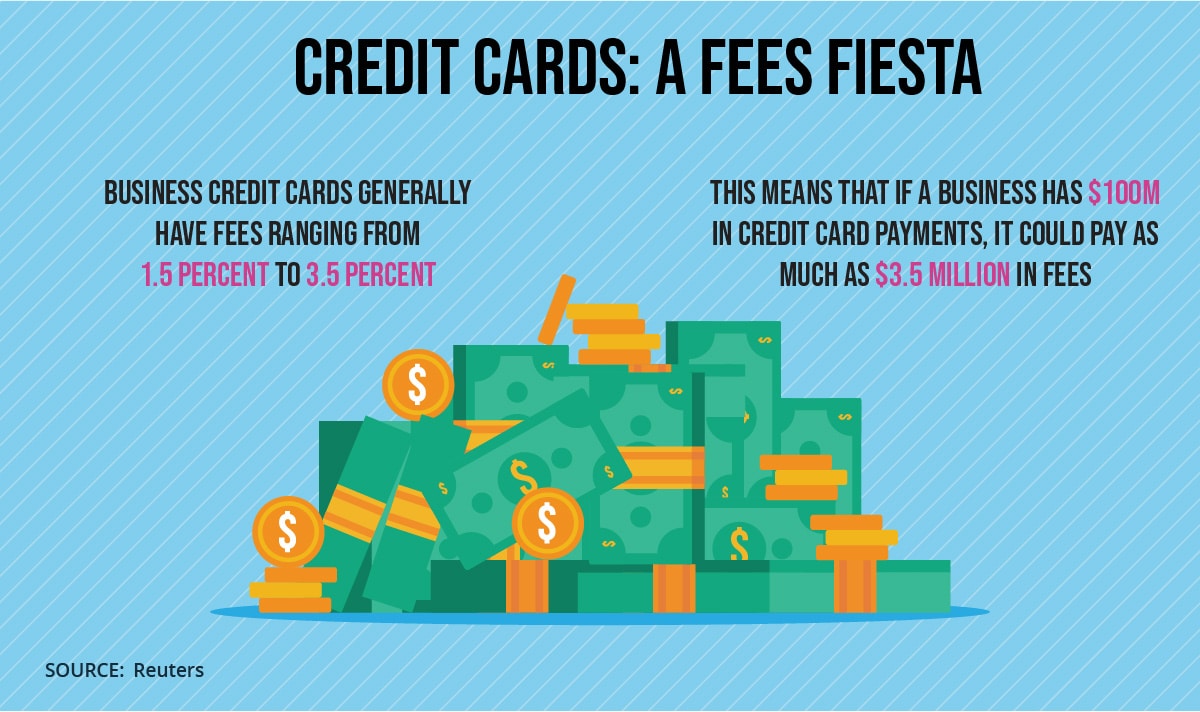

So why do some businesses shun credit cards, be it from Visa, Mastercard, American Express or whoever? For one thing, while credit cards can be convenient and come with rewards, they aren’t cheap to use, with Reuters noting in February 2022 that fees generally range 1.5 percent to 3.5 percent. This means that if a business makes $100 million in payments via credit card, it’s looking at paying anywhere from an extra $1.5 million to $3.5 million in fees.

High fees can be devastating for business credit card use, with Stampli and Treasury Webinars noting in its payments study: “Most existing research would suggest that companies make decisions regarding how they make payments based on payment type costs.”

Now, fees can be justifiable, but traditional charge cards have other issues, too. They come with fixed dollar amounts that can be used by anyone who has access, typically until a monthly limit is hit. With business credit card limits sometimes above $100,000 and often in the range of several thousand dollars, it’s easy for fraudulent charges to accumulate well before auditing or reviews of expense reports will bear them out.

Bottom line: Credit cards have enough issues associated with them that it’s smart to have other payment methods lined up.

Why P Cards are Worth Learning About

P cards, or purchase cards (or procurement cards, as they’re known in the United Kingdom) are far newer on the scene than credit cards, with some key, positive differences.

Unlike credit cards having fixed dollar amounts, P cards, which are similar to virtual or ghost cards, can be generated with unique numbers and preset spending limits for each transaction. This can keep card numbers from being used for unauthorized purchases if they fall into the wrong hands. At the end of the day, there are few forms of payment as secure as P cards.

Virtual cards like Stampli Card can also integrate with AP automation systems, matching with purchase orders and more, which can help firms have the most accurate data. Accounts payable data has become increasingly valuable, with Oracle NetSuite noting in 2020, “It’s pretty well established that finance leaders are continually striving to use data more effectively, with an imperative to produce better reporting on key performance indicators (KPIs) and identify areas to realize cost savings across the business.”

P cards coupled with AP automation are a powerful tool for helping businesses get the KPI reporting they need.

As of right now, businesses appear to be using credit cards far more often than P cards. In Stampli and Treasury Webinars’ payments survey that noted 36% of companies preferring to pay suppliers via credit card, just 4% preferred to pay by virtual or ghost card.

In general, virtual payments are still in the early phase of adoption in the business world. Still, it’s already clear that there can be times where a company would be smart to consider using the right P card.

Credit Cards and P Cards: When to Use Each Payment Type

Credit cards and P cards, like any payment method, have a few primary guiding factors for why they get used.

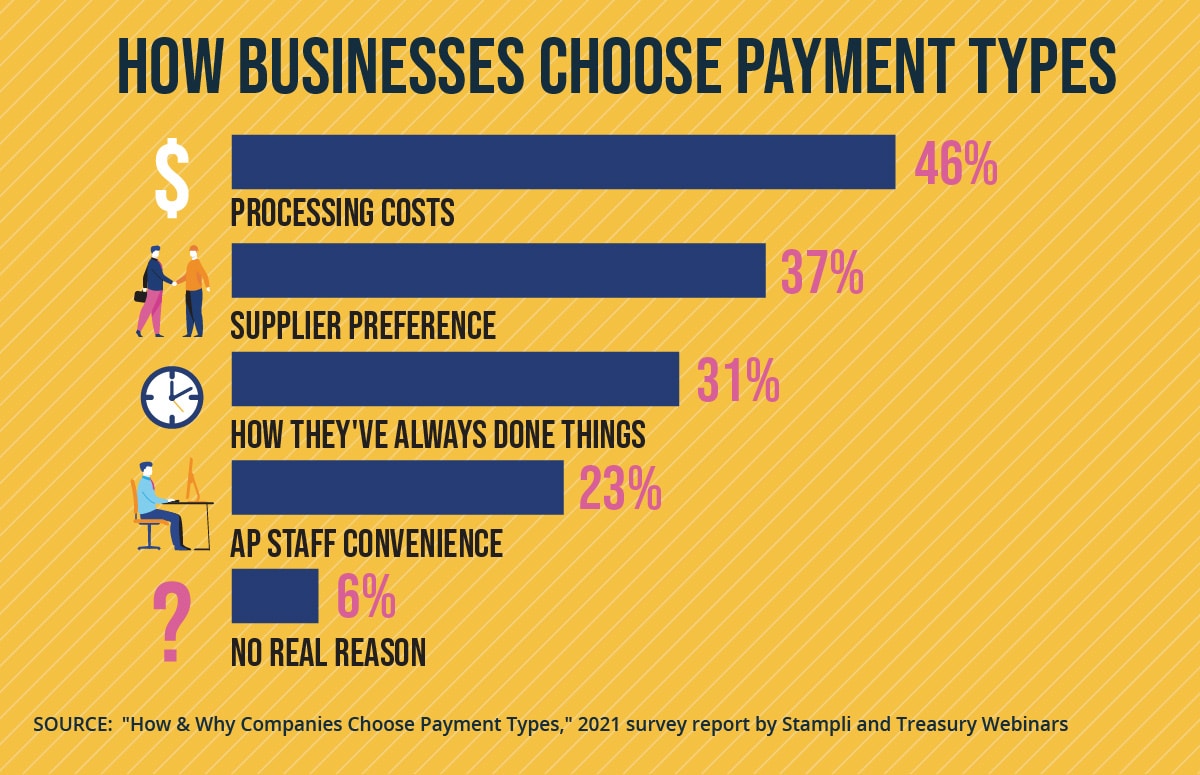

Stampli and Treasury Webinars’ payment study asked why companies preferred to pay by specific methods, letting respondents list as many factors as necessary. The study found:

- 46% of respondents were guided by processing costs (which could help to explain the popularity of low-fee methods like the ACH, with 29 billion payments made through that network in 2021);

- 37% were motivated by supplier preference;

- 31% said they’d always done things this way;

- 23% cited AP staff convenience;

- 6% said there was no real reason.

That said, beyond the standard factors for making payments, there are optimal situations for using credit cards and P cards. Let’s look at each:

1. When to Use Business Credit Cards

Businesses often will need financing and sometimes a loan from a bank or the U.S. Small Business Administration isn’t the easiest to come by.

Credit cards can be a form of microfinancing, provided that businesses understand the debt they’re taking on. U.S. News & World Report noted that the average minimum APR for business cards was 14.22% as of December 2021. At that rate of compound interest, $1,000 in principal could become $1,944.06 in just five years.

Accordingly, business credit cards are best used by companies that know they’ll be able to quickly pay their bills, with credit cards allowing them a kind of bridge financing. This isn’t the only benefit, of course, with credit cards also able to help companies build their credit scores and earn rewards.

But at their core, for better or worse, credit card payments allow businesses to spend money whether they have it or not.

Optimal times to use business credit cards

Credit cards can be good for times of slow or delayed cash flow when payments still need to be made. Credit cards are also a tool for when a business is looking to build its credit score or when suppliers request this form of payment.

2. When to Use P Cards

Sometimes, businesses want the benefits of credit cards without the drawbacks of cards. Companies might want remote team members to be able to make whatever payments they need without opening the door to possible fraudulent purchases. Or businesses might want to be able to make digital payments without taking on high APR debt that’s common in credit transactions.

For these reasons and more, P cards can make a fine alternative to business credit cards. P cards mix the benefits of credit cards, which include convenience and the chance to earn rebates, with the security and benefits of other payment methods.

One other big difference we should note between credit cards and virtual cards, is that the latter often must be paid off in full at the end of each month and sometimes require money to be deposited in advance by businesses. But a purchasing card program can be a good thing for companies, helping them avoid spending money they don’t really have.

Optimal times to use P cards

Like credit cards, P cards are great for remote or distributed team members, and P cards can help businesses pay for travel and entertainment (T&E) expenses and much more. P cards are also good for companies with AP automation systems, as the cards can record a lot of different transactional data and sync it directly into a firm’s accounting system.

Why to Make Payments with Stampli Card

For companies ready to add an emerging form of payment to their repertoire, here are a few things that Stampli Card brings to the table.

Available When and Where You Need It

The past couple of years with the COVID-19 pandemic have shown many things, including that there will be times when it will be difficult, if not impossible, for businesses to meet in person. In these scenarios, it won’t always be easy or advisable to try to cut paper checks for employees who need to make payments or to provide them with credit card numbers to use.

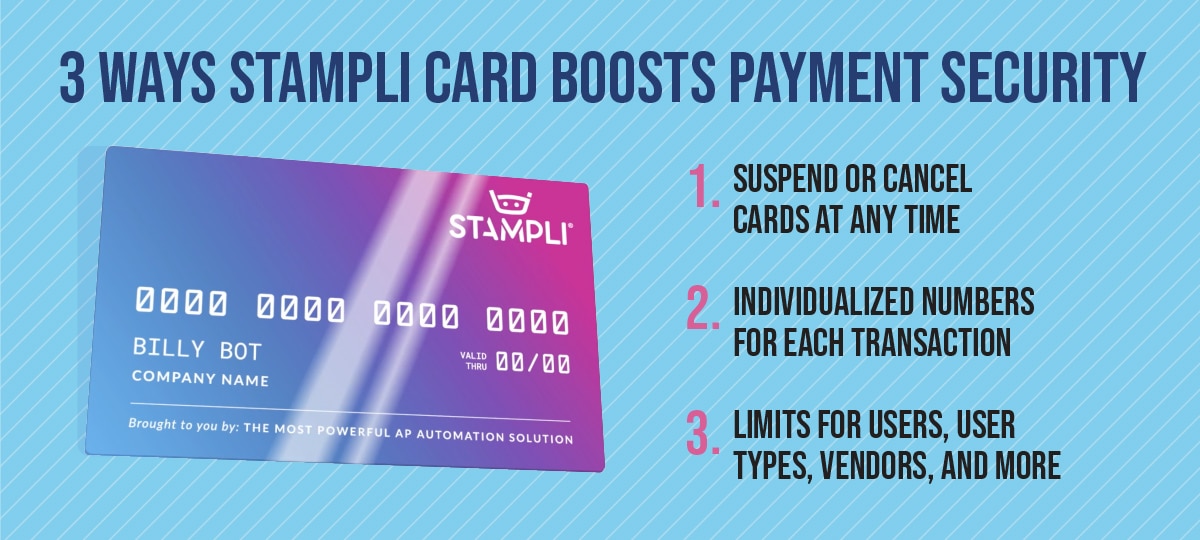

On the other hand, businesses can easily produce an unlimited number of individualized Stampli Cards for any employees that need them, regardless of where they may be. Card issuers within companies can create Stampli Cards instantaneously as soon as individual employees are approved.

Great Payment Security

With Stampli Card, there’s no tense worry for businesses about what will happen when a credit card statement arrives or if some phantom or forgotten check clears. Instead, companies can control their spending before it occurs, offering outstanding payment security.

Aside from customized numbers and precise limits on spending with each card, companies can also set limits for user types and vendors. In addition, Stampli Cards can be suspended or outright canceled at any time, keeping companies from having to worry about which cardholders might have unauthorized access to payment information.

A Tool to Create Better AP Data

There’s no guessing or wondering with Stampli Card. Companies will have real-time expense management insights that will guide them toward better decisions.

All in all, it’s just one more reason that while P cards might not be as frequently used as business credit cards, implementing a card program for them is absolutely worth considering. It’s a streamlined payment process, easy reconciling, and much more.

Payment needn’t be hard. Sign up for Stampli Card.