B2B international payments guide: manage FX risk and fuel business growth

In the hypercompetitive global marketplace, mastering international payments is crucial to business growth.

In this guide, we’ll help you navigate international transactions and make informed decisions about paying overseas vendors. We’ll explore trends that are transforming global payments from a system that seemed hopelessly stuck in the Stone Age into a powerful way to maintain healthy supply chains and positive cash flow.

Read on for strategic insights on how you can leverage electronic payment methods, prevent fraud, integrate payment systems, manage FX risks, and strengthen vendor relationships to transform the way you manage international payments.

What are cross-border B2B payments?

A B2B international payment is when you transfer money between businesses residing in different countries. For a simple example, consider international trade. Your company, based in the US, buys a software package from a company based in the UK. The UK company sends you an invoice, you pay the invoice in the chosen currency using an international payments provider or your bank, and then the UK company receives the payment.

International payment methods

There are several ways for businesses to make international payments. Here are the most common payment options:

- Wire transfer: International wire transfers are the most common payment method. A wire transfer is a money transfer between two companies’ bank accounts. Most wire transfers are sent via SWIFT, a secure international bank messaging system.

- Paper checks: Mailed checks are used for transactions where the receiving country’s banks honor checks from the sending country, such as Canada and the US.

- Global ACH: An electronic payments service based on the automated clearing house system in the US. It provides fund transfer capabilities using the US ACH system and similar electronic funds transfer systems in other countries.

- Foreign currency business account: A business can open a foreign currency account with a foreign branch of their own bank or with a foreign bank and then fund and transfer payments from that account to pay vendors.

- Credit cards: Virtual cards let businesses make international payments instantly but may only be available or accepted in some countries.

- Digital wallet: Payment providers like PayPal offer fast electronic international transfers to vendors in supported countries.

About currency exchange rates

International payments can be made in any currency, although both parties usually agree on the buyer’s or seller’s local currency. In our US/UK transaction above, the buyer and seller could conduct the transaction in US dollars (the buyer’s currency) or British Pounds Sterling (the seller’s currency). Depending on which currency they choose, one of the parties will need to convert the foreign currency into their own.

For instance, if both companies choose to do business in USD, the US company will pay the invoice in USD, and the payment provider or bank will convert the funds to pounds sterling and pay the UK company. Alternatively, the US company could choose to pay the UK company in pounds sterling, in which case the US company’s bank would convert the payment amount from pounds sterling to USD and debit the US company’s bank account by that amount.

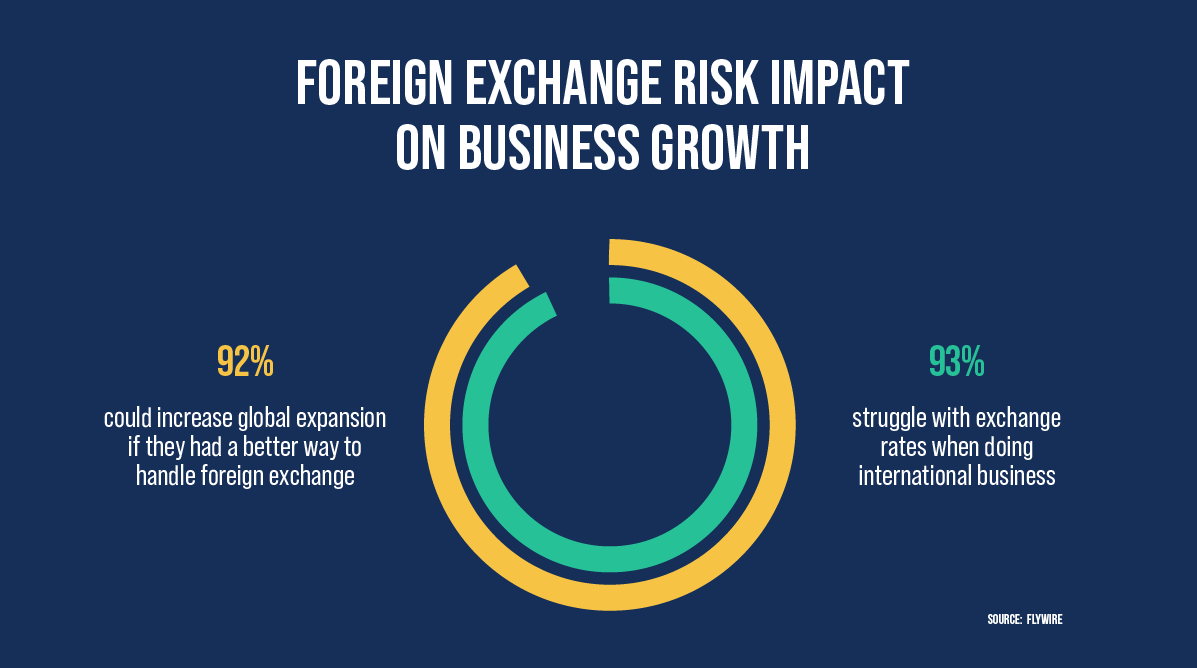

Managing foreign exchange rates is only one of several challenges your business may experience as you begin making international payments. Let’s look at the most common challenges and then explore how your business can overcome them.

B2B cross-border payments challenges

Businesses making international transactions face some of the same challenges as domestic payments, and a few unique to B2B cross-border transactions. Here are the main challenges you might encounter.

Payment speed and certainty

“Cross-border payments are often fraught with time delays, hidden fees, and bounce backs. … a labyrinth and complete mess to deal with.”

– Lawrence, CFO

Prompt and certain payment is crucial to international business. However, several factors could contribute to late or missed cross-border payments.

- Slow international payments process: Your internal process for processing and approving international invoices may get bogged down as your AP team. manages currency differences and international payment systems, especially if your business relies on manual processes.

- Intermediary delays: International payments usually involve multiple intermediaries, such as payment processors and banks, which can add delays and complexity to the process.

- Errors and omissions: Errors in regulatory or banking information or transaction details, such as SWIFT codes, can lead to delayed, misrouted, or incomplete payments.

Payment methods: Different countries may restrict or prioritize specific payment methods, which may cause payment delays.

Currency risk

“Any time we have to work with an out of country vendor with other currency, it is always a challenge as you are paying a literal moving target.”

– David, CFO

Changes in foreign exchange rates can expose your business to significant financial risk during currency conversions.

Let’s use our US/UK software example to explain. Say both companies agree on USD for the transaction, and the price of the software is £10,000. Suppose the US dollar is trading at $1 = £0.79 (or £1 = USD 1.27) when the contract is signed, so the price is USD 12,700. However, by the time the US company goes to pay the invoice, the exchange rate has changed to (or £1 = USD 1.05), which reduces the USD price to $10,500. If they aren’t aware of the change in the exchange rate and don’t recalculate what they owe, the US company will pay $2,200 too much for the software.

Exchange rate fluctuations are determined by world events — and beyond the control of businesses. Businesses often hedge against exchange rate exposure, but that adds more complexity to international transactions. Since international suppliers usually want to be paid in their own currency, businesses need to control foreign exchange risk as much as possible.

International transaction costs and regulatory risk

“International payments are confusing and normally have a lot of hidden fees.”

– Carol, CFO

International transactions can be pricey. Hidden transaction fees, like wire transfer and intermediary fees, can increase costs for buyers and sellers. These unpredictable fees are often high — sometimes even exceeding the agreed-upon total cost for the transaction.

Regulations and taxes vary from country to country, making it difficult for businesses to comply with the rules and predict their tax liabilities on international transactions. Companies must be aware of all fees involved in international payments so they don’t overpay or underpay an invoice.

Risk of fraud

“Information gaps are the key for us.”

– Doug, CFO

Wire fraud is an ever-present risk in international transactions. Fraudsters can impersonate suppliers or buyers, forge payment details or intercept payments, or infiltrate AP and AR departments and generate fraudulent transactions. Businesses need to understand the tactics used by criminals and have the data and transaction visibility to detect and prevent fraudulent activities and protect themselves from international payments fraud.

Vendor management

“The biggest problem encountered by our organization with respect to international payments is vendor frustrations. There is far too much back and forth as opposed to the simplicity of dealing with domestic vendors. The whole process needs to be simplified.”

– Monica, CFO

Having up-to-date, relevant, and accurate vendor information is important when making B2B international payments. Without the correct information required for international transfers, such as bank account numbers, transit numbers, SWIFT codes, payment terms, and supplier names and addresses, businesses run the risk of delayed or incomplete transactions. They can also be exposed to fraud by criminals using fake transaction details to divert payments.

Understanding the various bank, regulatory, and documentation requirements for international payments can be challenging, especially for businesses that manually track and store vendor information.

Integration with business systems

“International payments are a pain and not streamlined. There is lack of integration with ERP. Even though there are several payment options, most transactions are handled using wires that have to be set up on the bank side. The reconciliations are very manual and a waste of human resources.”

– Anil, CFO

A lack of integration between external bank payment gateways, ERPs and accounting systems, and accounts payable systems complicates transactions, delays payments, and exposes companies to fraud and errors.

Flipping back and forth between disconnected systems to view vendor details, invoices, and relevant data can frustrate AP teams and create a lack of transparency. Additionally, manual processing can bog down as transaction volumes grow, creating further delays and frustration.

By understanding how these challenges can affect international transactions and implementing strategies to protect your business from them, you can set your business up for success and avoid potential pitfalls. Let’s look at a few ways to improve B2B cross-border payments.

How to improve B2B cross-border payments

Improve payment process transparency

You can’t manage what you can’t see. Complete visibility into your international transactions lets you identify problems, anticipate risks, and forecast transaction costs. Consider payment processing solutions that track and record transactions and synchronize payment data with other business systems to ensure a single source of truth.

Reduce unnecessary fees and protect against FX risk

Explore payment solution providers who cut out unnecessary intermediary fees, provide fee transparency, and protect against foreign exchange risk to reduce the cost of international transactions.

Invest in AP automation

Accounts payable automation streamlines invoice and payment processing and provides data transparency. With the right solution, you can pay international vendors faster and reduce processing costs. Increased data transparency also helps you reduce human error and prevent payment fraud.

Manage vendor documentation

Collect and store vendor documentation like vendor details, contracts, certificates, and banking information in a centralized, easy-to-access location. By managing vendor information, you can reduce payment errors and delays. Consider investing in an automated document management solution or an AP automation system that features a vendor portal to streamline vendor onboarding and document management.

Implement an international payment solution

Manual data entry and payments processing is expensive, error-prone, and slow – leaving you at risk of late payments and exposed to currency fluctuations and fraud.

An automated payment processing solution replaces manual workflows and streamlines your payment processes. Look for a solution that manages domestic and international payment workflows, unites international payment types into one platform, seamlessly integrates with ERPs and accounting systems, and mitigates foreign exchange risk. The right solution will be flexible to adapt to your existing workflows, manage multiple currencies and jurisdictions, and scale to meet your growing business needs.

Stampli Direct Pay: International payments built for the modern era

“International Payments built for the modern era of AP seem much more efficient especially when everything syncs with ERP. Any efficient digital workflow process that provides the necessary processing information upfront allows for more controls.”

– Carol, CFO

International Payments from Stampli Direct Pay lets you pay international suppliers as easily as domestic suppliers. Make B2B international payments with the same workflows and controls as domestic payments — all without leaving your accounts payable system. All payment records automatically sync back to your ERP while maintaining a complete audit trail in Stampli for easy reconciliation.

Now, you can pay vendors across 100+ countries using international wire or international ACH, in USD or local currency, in a matter of days — and save money with a new approach to FX risk.

One system for accounts payable and international payments

International Payments is a unified solution for managing AP automation and executing global payments. It ends the need to juggle between your AP system, bank, and ERP, simplifying workflows and setting the foundation for error-free and time-effective financial operations.

Complete visibility and control

All crucial information — invoice details, vendor data, and more — are at your team’s fingertips as they process global payments. International Payments features a centralized hub for all payment-related information, so you no longer have to sift through multiple systems. Not only does this speed up payment times, but it also enhances visibility and control over transactions.

Advanced vendor management

International Payments features an integrated advanced vendor management platform that fosters a collaborative environment between your business and your vendors. Vendors can independently upload and maintain their documents and information, significantly reducing the administrative burden on internal teams.

FX rate transparency and management tools

International Payments from Stampli provides clear visibility into real-time FX rates, so you know the exact rates you’re paying. This transparency allows for better cost management, accurate budgeting, and informed financial decision-making.

International Payments also features a revolutionary new hands-off approach to managing FX rate impacts on international payments. You can build custom payment workflows in International Payments that can be triggered by specific FX rate goals and targets.

For example, you can set a desired FX rate threshold, and Stampli will execute payments when those conditions are met. This capability is not available anywhere else in the industry — patents are pending!

Industry-leading payment capability from the leader in AP automation

International Payments eliminates the gap between your AP and payments systems that disrupts your workflows and weakens control.

It’s time to take control of B2B international payments

Technological transformation has finally reached the realm of international payments, and it couldn’t have come too soon.

If you’re interested in seeing how Stampli Direct Pay seamlessly integrates your payments workflow with accounts payable and your ERP, you should contact us to request a demo.