Virtual Card vs. Physical Card: When to Use Each With Stampli

It used to be that whenever businesses made a payment by card, there was no question they’d be using a physical card.

It’s safe to say this is changing.

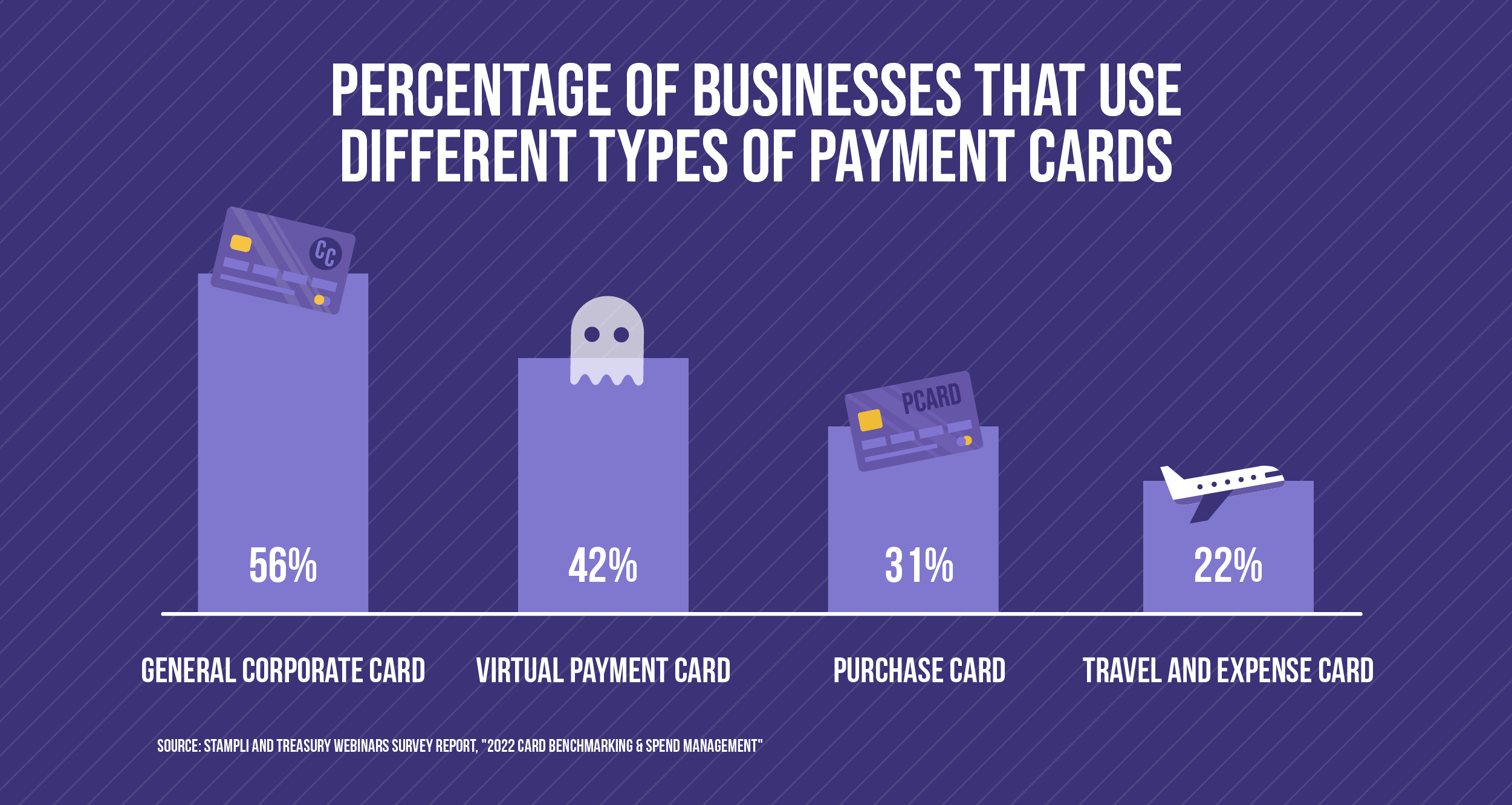

A recent survey by Stampli and Treasury Webinars, “The 2022 Card Benchmarking & Spend Management Survey Report” asked respondents how often they used different types of cards. It found that while 56% of people surveyed had used general corporate cards, 42% had used virtual or ghost cards.

At Stampli, we are payment-agnostic, and we don’t believe in right or wrong payment methods, just different situations that might suit certain payment types. As this podcast episode points out, cash management requires detailed planning. Today, we’re going to look at when to use physical and virtual cards and how Stampli Card has evolved in each space.

The Basics of Physical and Virtual Cards

When a company makes a payment, they’re most likely to do so by card. Until recent decades, this has often meant using a physical credit card; and even now, physical cards remain vastly preferred in business. A 2021 survey report by Stampli and Treasury Webinars, “How & Why Companies Choose Payment Types” found:

- 36% of companies preferred to pay suppliers by credit card;

- 30% preferred checks;

- 24% preferred the automated clearing house, or ACH;

- 4% preferred virtual or ghost cards;

- 6% expressed no preference.

Other sources have also shown credit cards to be a common form of payment, with PYMNTS.com noting in 2021 that 48% of businesses were paying bills with credit cards. (This doesn’t necessarily include debit cards, which businesses can use for ATM withdrawals.)

Credit cards are popular for various reasons. Stampli and Treasury Webinars’ benchmarking study noted that companies tended to be driven toward making payments with cards due to any of the following:

- Processing costs;

- Chance to earn rebates;

- A greater number of automated controls;

- Superior spend reporting;

- Customer preferences;

- The fact that it was how they’d always made payments.

Credit cards also help businesses optimize cash flow, since companies can make payments before having to come up with the money. Cash flow is critically important to B2B companies, with Payments Journal noting in August 2022, “When payments are delayed, it can have a ripple effect on cash flow, leading to late payments to suppliers, delays in payroll, and other financial problems.”

Simply put, credit cards can help businesses avoid problems, provided of course they’re used responsibly.

Why Cards Have Been in Physical Form Until Recent Decades

Various factors have helped keep a majority of payment cards in physical form in the business world.

One issue is slowness to accept change. When it comes to paper checks, despite long standing issues – such as processing costs, the time it takes for checks to arrive, and the risk of fraud – checks remain common for B2B payments. PYMNTS noted in March 2022 that 81% of companies were paying other businesses with checks and 40% of all B2B payments were made with checks.

The payment study from Stampli and Treasury Webinars also noted there had “been quite a bit of hype from AP and payment automation solution providers over the last three years focused on how virtual and/or ghost card can be a means for companies to mitigate payment cost and even turn accounts payable into a profit center.”

But 60% of respondents said virtual card programs fell short of what was promised. Clearly, more innovation has been needed in the virtual payment space and companies like Stampli have been moving to meet the need.

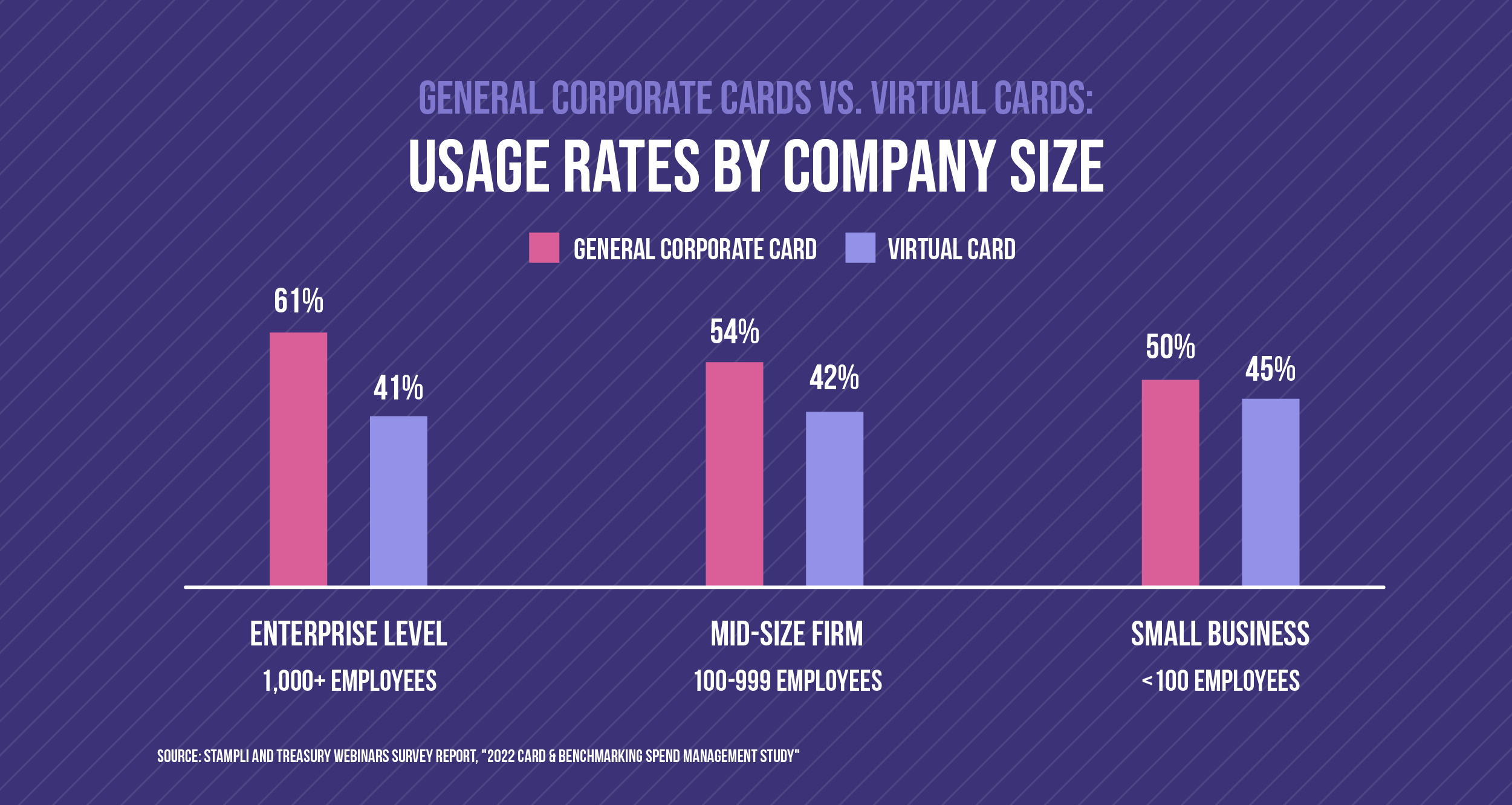

Stampli and Treasury Webinars’ benchmarking study noted something worth considering, too: While usage rates of general corporate cards increase with company size, usage rates for virtual cards decrease with company size. Whether it’s due to bureaucracy making it harder to implement virtual cards at enterprise firms, or small businesses being more likely to be shut out of traditional forms of credit, virtual cards tend to be more common at smaller companies.

How Virtual Cards Came Onto the Scene

In different forms, virtual payment cards have been around for close to 20 years, with CNET noting in January 2022 that the first contactless cards were issued in 2004.

The same article noted how mobile computing has furthered contact-free payments, with Google debuting a virtual wallet (now known as Google Pay) in 2011 and Apple doing the same (with what’s now known as Apple Pay) the next year. Digital wallets have only grown in use since then, with the COVID-19 pandemic unsurprisingly driving a surge in digital payments.

The virtual payment trend could be intensifying, too, with PYMNTS noting in October 2021 that “We are seeing virtual cards become the next go-to for consumer purchases.” Juniper Research has projects that virtual card transactional value could reach $5 trillion by 2025, more than tripling from 2020.

It’s easy to see why virtual cards are growing in popularity. Virtual or ghost payment cards, also known as single-use credit cards, were “created with the goal of making online shopping safer,” according to Investopedia. Virtual cards like Stampli Card make it so that businesses can print individualized cards with unique numbers, specified users, and payment amounts for every transaction.

Determining Whether to Use Physical or Virtual Cards

Stampli and Treasury Webinars’ benchmarking study included a question asking people why they chose particular payment types. Interestingly, it found that more respondents than any other, or 33% said they were doing things the way they’d always done them with particular vendors or suppliers.

To some extent, this makes sense, with businesses perhaps not wanting to rock the boat with certain product or service providers who might prefer obscure payment types (penny rolls, anyone?) But we’re here to say both that vendors can be brought onboard with emerging forms of payment like virtual cards and that there will be situations that call for innovative forms of payment.

Here’s how to parse between using physical and virtual cards.

Option No. 1: Physical Cards

Sometimes, it makes sense for companies to stick to using physical cards for payment. Perhaps the company is doing business with a more established or old-fashioned client who’d have no problem processing a plastic card with a Visa, Mastercard, or American Express logo on it, but who might get thrown if a virtual card is presented.

Granted, vendors can be brought up to speed on virtual cards, with Stampli and Treasury Webinars’ payments study noting that 63% of companies had programs to get their suppliers to take virtual payments and that 67% of companies had AP automation firms (such as Stampli) that could help them make the change. Still, the conversion programs take time.

There’s a convenience factor, too. Not every retailer or other business takes virtual cards, at least not yet, with credit reporting giant Experian noting in October 2021, “Physical cards are almost universally accepted when you’re paying in person, whereas you can’t offer a virtual card number to pay for your restaurant check.“

Sometimes, a business person will just need to have a credit card in their wallet or at least have credit card numbers available from their department that they can use when the time arises.

When to use physical cards: Even businesses that see the benefits of virtual payments might want to keep a credit card or two on hand for certain situations.

This can include dealing with clients who prefer traditional credit cards and traveling in areas without broad acceptance of virtual cards but where in-store purchases might need to be made. Credit cards can also be good for subscriptions, since these can pull from the same account information each month.

By no means do credit cards have to be used for every payment, but they’re a generally serviceable option to have available.

Option No. 2: Virtual Cards

Virtual cards are a great payment option, because for all the conveniences of credit cards, they have their drawbacks, too. One of the weak points is spend control, and there are several reasons why.

First, aside from the limits that financial institutions assign to credit cards, it can be tough to get individual employees to adhere to spending limits on physical cards. Assigning spending limits for credit cards may be an uncertain process in the business world. In Stampli and Treasury Webinars’ benchmarking study, it found that card spend limits were set by the following:

- By department 42% of the time;

- By service type 32%;

- By product type 26%;

- By MCC (merchant category code) 21%;

- By fiscal quarter 18%;

- By month 17%.

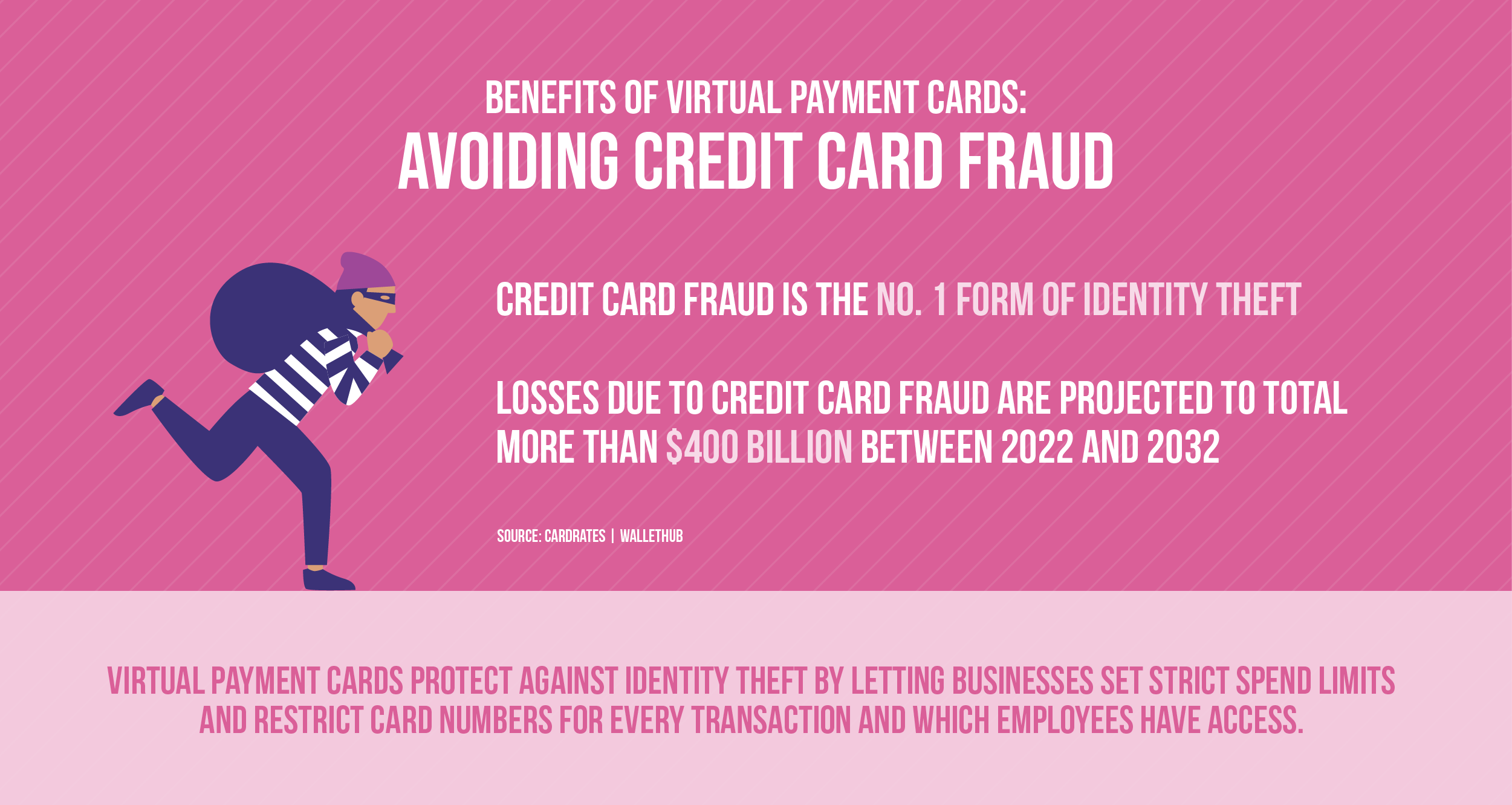

With their set numbers, physical credit cards are also susceptible to security risks such as fraud – the most frequent form of identity theft, according to a Federal Trade Commission report. In the coming decade, credit card losses because of fraud could reach more than $400 billion. It can be hackers in data breaches or anyone else who gets hold of 15 or 16-digit numbers of credit cards wreaking havoc.

On the other hand, virtual cards like Stampli Card provide an extra layer of security. Companies get strict spend and user limits that they can set with every transaction, controlling which users can use cards and precisely how much they’re allowed to spend. A new unique set of numbers can also be issued for every transaction with virtual cards.

It’s also worth noting that major financial institutions seem to be grasping the security benefits of virtual cards and are now offering virtual credit cards.

When to use virtual cards: If there’s any concern whatsoever about security, virtual cards can be a great way to go for payments. Accordingly, virtual cards can be ideal for online payments and e-commerce purchases.

Making Payments With Stampli Card

For people uncertain whether they want to make payments with a physical or virtual card, good news: It’s possible to do both with Stampli Card.

Stampli Card: A Customizable Payment Solution

After beginning by creating a state-of-the-art AP automation platform that uses artificial intelligence and machine learning to help companies process invoices faster, cheaper, and with greater accuracy, we realized that it made sense to also give companies a faster way to pay bills.

One of our innovations in the payments space has been Stampli Card, which debuted in recent years as a virtual payment card option.

Stampli Card gives AP teams centralized and customizable spend management controls. Companies act as the card issuer, determining which employees can be issued cards. The cards function similarly to prepaid cards in that cardholders are limited to spending precise amounts designated for transactions.

Not only is the card a breeze to use at checkout, but card information is easily available for real-time analysis and reconciliations.

Make Stampli Card Payments in Stampli Direct Pay

We’ve now integrated Stampli Card into Stampli Direct Pay, which already allows companies to make ACH or check payments through our AP automation platform.

Now, companies can handle invoices directly with Stampli Card to code, approve, and pay vendors. The process makes vendor payments faster than ever. We’re also happy to provide partner companies with incentives like rebates and rewards.

In business, customers have more payment options than ever before. We want to do everything we can to ensure that companies can make physical or virtual card payments anytime.

Pay okay, that’s the Stampli way. Try Stampli Card in physical or virtual form today.