How to make ACH vendor payments

Do you want a fast, reliable, and low-cost way to pay suppliers?

Many businesses use Automated Clearing House (ACH) transfers instead of paper checks or wire transfers to pay their vendors. ACH business payments have several benefits for your business, including:

- Cost savings: ACH payments cost approximately $0.25 to $5, much less than paper checks or wire transfers.

- Efficiency: Standard ACH payments take one to three business days, and Same Day ACH payments can be completed in a single day – much faster than checks.

- International reach: Global ACH allows fast and inexpensive payments to international vendors.

- Integration: Most ERPs, payment processors, and accounting systems integrate with the ACH system, making it easier to track payments.

- Security: To prevent payment fraud, ACH payments are sent and received according to strict security standards.

In this article, we’ll talk through the basic steps to set up ACH and make an ACH payment to a vendor. We’ll also discuss choosing the right payment solution to leverage ACH and EFT payments for your business.

What is an ACH payment?

The ACH Network is an electronic funds transfer (EFT) system that connects US banks, credit unions, and financial institutions to facilitate the sending (ACH debits) and receiving (ACH credits) of funds between accounts. The ACH payment system provides a secure and fast way to make digital payments. Businesses and individuals made 31.5 billion ACH payments valued at $80.1 trillion in 2023.

In a nutshell, ACH acts as a secure channel for transferring money between accounts at two different financial institutions: the Originating Depository Financial Institution (ODFI) and the Receiving Depository Financial Institution (RDFI). Examples of ACH payments include paying suppliers, making direct deposits, and accepting payments from customers.

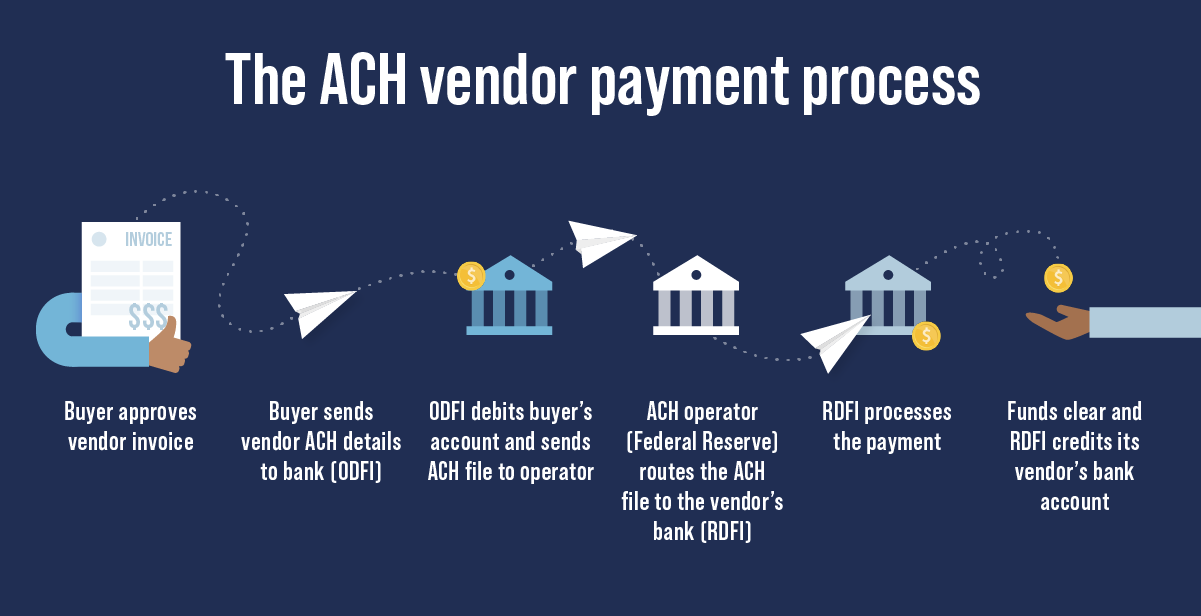

For example, ACME Manufacturing wants to make an ACH transfer to its supplier, Wiley Consulting. The transfer takes five steps:

- ACME tells its bank (the ODFI) the transfer amount and provides the banking details for Wiley Consulting.

- ACME’s bank debits the amount of the payment from ACME’s account.

- ACME’s bank sends a file with the transaction details to the ACH Operator (the Federal Reserve or Electronic Payments Network).

- The ACH operator routes the file to Wiley’s bank (the RDFI).

- Wiley’s bank credits Wiley’s account with the transfer amount.

To get started making ACH payments to vendors, you need to choose an ACH provider (your ODFI) and a payment processing solution.

How to select an ACH provider

Your ACH provider services as your ODFI — they process your payment requests and execute ACH transactions. Generally, the ACH payment processor is your bank, but can include other financial institutions. Some payment processing software solutions also offer ACH payment services through payment partners. It helps to shop around and look at various solutions and pricing models to find the best fit for your business.

Criteria for choosing an ACH provider

There are a few things to consider when choosing an ACH provider. First, confirm the provider is Nacha-certified to ensure they comply with standards for sound core practices in ACH payment processing.

Next, evaluate the provider’s capabilities. Look at the level of support they offer, their transaction fees, and transfer times. If you use an ERP, accounting software, or payment processing software, check how it integrates with the payment provider. Finally, check user reviews to see what other businesses say about the ACH providers you’re considering.

How to choose an automated payment processing solution

A payment processing solution streamlines the vendor payment process by automating manual workflows and tasks, including:

- Ensuring invoices are approved before payment.

- Managing vendor information.

- Unifying payment types (check, ACH, wire transfer, credit cards) on a single platform.

- Recording payments in the general ledger.

- Making vendor payments.

- Integrating with banks and ACH providers.

A standalone payment automation solution provides maximum flexibility and freedom in what payment methods you choose and how you manage payment processes. Choosing the right automated payment processing solution offers significant advantages in vendor document management, payment handling, and transaction tracking.

Criteria for choosing a payment processing solution

The primary criteria for choosing the right payment processing solution are capability, compatibility, and cost-effectiveness. Look for solutions that offer multiple payment options and user-friendly design, integrate well with ACH providers and business systems, and help reduce processing costs and time for your team.

Once you’ve chosen an ACH provider and payment processing solution, it’s time to set up and start paying vendors.

Setting up to make ACH payments

Setting up ACH vendor payments is a two-step process.

Step 1: Set up ACH payments in your payment system

Start by adding your banking information to your payment processing system. Obtain your ACH provider’s ACH specification sheet, then enter the information in the appropriate section of your payment solution. For example, in Sage Intacct you would enter ACH banking information under ACH bank configurations.

After entering and verifying the banking information, you’re ready to begin making ACH payments.

If you are using your bank’s payment portal, this information is already provided, so you can skip this step and follow their onboarding process to learn how to start making vendor payments through the portal.

Step 2: Set up ACH payments for vendors

To start making ACH payments to your vendors, you’ll need to get their banking details and enter them into the vendor profile in your payment system. The banking details include:

- Vendor name

- Vendor address

- Tax ID number

- Financial institution name and address

- Bank account number

- ACH routing number

- Contact details

You can get your vendors’ banking information by contacting them via email or phone and manually entering the data in your payment system. Alternatively, payment automation solutions like Stampli Direct Pay offer several ways to obtain vendor payment details, such as:

- Request vendors to enter payment details directly via a vendor portal.

- Import vendor payment details from your ERP or accounting system.

- Upload a file with vendor payment details.

Getting permission

You should also get permission from your vendors to pay them via ACH transfers. Permission can be a formal payment agreement or a simple email from the vendor agreeing to ACH payments. The key is to get it in writing. When you get permission, it’s a good idea to store it electronically. Depending on how you obtain your vendor details, you can obtain permission via email or a vendor portal.

Once your bank information and vendor details are all set in your payment system, you can begin paying your vendors.

How to make an ACH payment to a vendor

In general, there are two options for making ACH vendor payments. You can make a single, one-time payment to a vendor, or you can pay multiple vendors in a batch. Some payment solutions also allow you to set up recurring payments.

Single ACH payment

The process of making a single ACH payment will differ depending on your payment solution. We’ll use Stampli’s process as an example.

Example: Single payment in Stampli Direct Pay

In Stampli Direct Pay, each vendor’s default payment method is set in their Vendor Payment Details. Once a vendor’s invoice has been approved, the AP clerk selects it and sends it for payment. Stampli sends the payment information to your financial institution (ODFI), and the payment is completed over the ACH network and credited to the vendor’s bank account.

Batch ACH payments

Some automated payment solutions send ACH payments in batches. Each solution has a different process. We’ll use Sage Intacct’s ACH payment process as an example.

Step 1: Select invoices to be paid

To begin, the AP clerk selects the bills they want to pay in Intacct’s Pay Bills function and then chooses ACH/Bank File as the payment method. Then, they select the bank they want to use to pay the bills, set the payment date, and send the bills for payment approval.

Step 2: Create the ACH file

After the bills have been sent for payment and approved, the AP clerk creates the ACH file to send to the bank. The ACH file contains the payment information and vendor details for all the bills. They do this by going to the ACH file generation function, verifying the payment information, and clicking Generate File to create the file.

Step 3: Send the ACH file

After the AP clerk generates the ACH file, they verify it and send it to the bank. The bank sends the transactions in regular daily ACH batches, and the payments are routed to the vendors.

Reconciling ACH payments

Reconciling your ACH payments lets you verify that transactions were made correctly. You can reconcile your payments by retrieving your bank statements and comparing them to your ACH transaction records in your payment solution. Note that many banks group transactions for batch ACH payments into a single debit transaction on your statement. Depending on your payment solution’s capabilities, you may need to manually match each payment transaction by hand to reconcile these transactions.

Tips for making ACH payments

There are a few things to remember when you’re paying vendors.

Payment processing cut-off times

Banks have strict cut-off times for ACH payment processing. If you send your payment request or ACH file after the cut-off time, your payment won’t be processed until the next business day.

Insufficient funds

Your financial institution will refuse your ACH payment request if you have insufficient funds in your bank account. Ensure that your account is funded before you pay vendors.

Transfer limits

Some financial institutions place limits on ACH transfers. Nacha limits same-day ACH transfers to $1 million per payment.

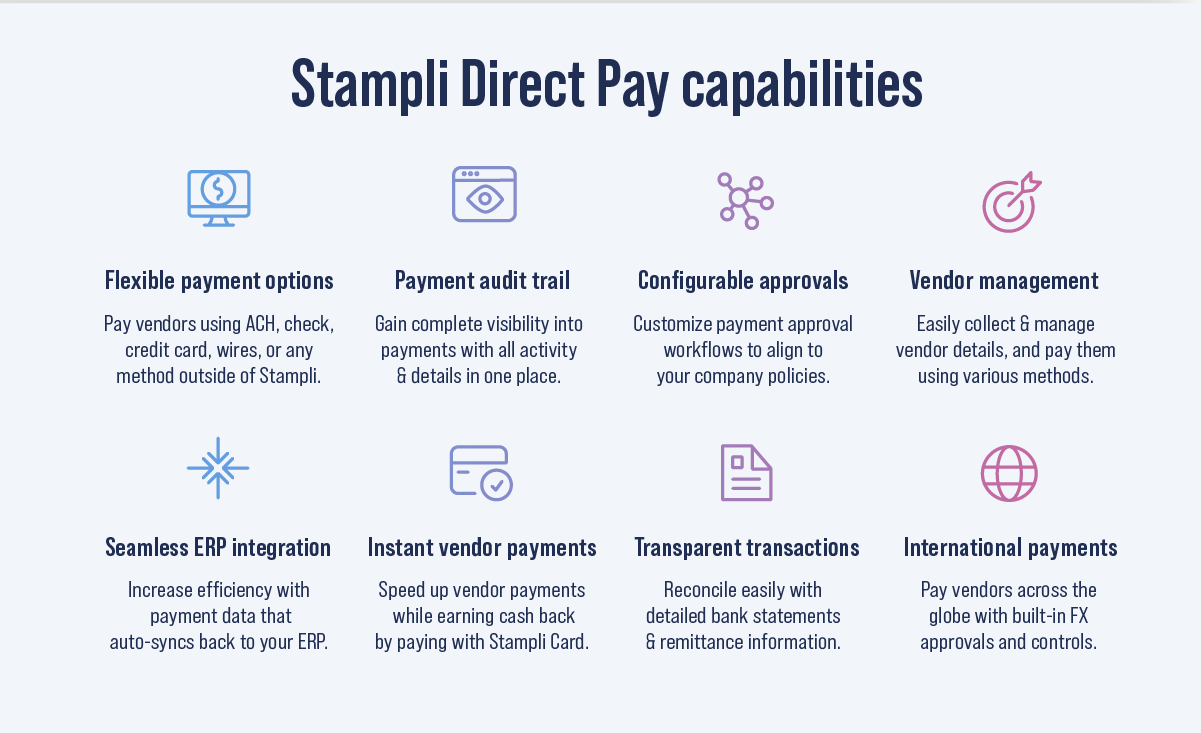

Stampli Direct Pay: A game-changer for accounts payable

Stampli Direct Pay is a payment-agnostic solution that extends your payment efficiency, visibility, and control over invoice payments. Stampli streamlines the entire payment process with easy access to all relevant details, offering maximum payment flexibility and controls. “The best [feature] so far is Direct Pay,” said one Stampli user review. ”This add on has allowed us to improve our AP processing time and the option of paying Vendors [by] ACH is great!”

“Stampli has been a game changer for our Accounts Payable department,” said another Stampli Direct Pay customer. “We used to spend countless hours processing invoices and cutting checks, but with Stampli, we can easily route incoming AP items for approval and pay them via ACH through the same portal.”

Direct Pay lets you fully control your vendor relationships without a middle party for your vendor payments. Seamless pre-built API or bridge integration with popular ERPs and accounting software means you can be confident that your entire company can access accurate real-time business transaction data when needed.

Here’s how Stampli Direct Pay gives you total control over ACH vendor payments:

Transaction-by-transaction withdrawal

After an ACH payment is approved, Direct Pay sends the payment information to ACH Network banks. You don’t need to download or upload ACH files to your bank or log into a separate system.

Easy ACH reconciliation

Other payment solutions create gaps in visibility that require manual efforts to resolve. Direct Pay lets you see individual ACH payments in your bank statement instead of a lump-sum debit. You’ll also be listed as the payer and your vendor as the payee, simplifying bank account reconciliations. As one Stampli customer says, with Direct Pay, you’ll “[e]specially appreciate the ACH payment process, the transactions post to our bank as individual transactions and not as a daily batch total which makes bank reconciliation fast and simple.”

Automatically collect vendor payment details

Stampli offers several ways to automatically collect vendor payment details, including via direct sync with your ERP or a vendor portal.

Payment-agnostic

Other payment solutions restrict your payment methods or force you (and your vendors) to use their preferred payment partners. With Direct Pay, you’re free to use whatever payment methods you wish.

Global ACH payments

Direct Pay lets you quickly send ACH payments to vendors in 100+ countries in their local currency.

Multiple entity support

You can use Direct Pay across multiple subsidiaries and set up related bank accounts per company.

Powerful vendor management portal

Vendors can provide payment information and documentation, set how they want to be paid, and check payment status with Stampli’s Advanced Vendor Management portal. Stampli’s Advanced Vendor Management helps you onboard new vendors efficiently, manage invoice and payment details, and collect required documentation like W9s, licenses, and insurance certificates to pay your vendors promptly while remaining compliant.

Own your vendor data

Stay in control of your vendor relationship, no middle man interference. All vendor data is owned by you, set internal controls on who can access it.

Direct ACH payments

Make ACH payments in Stampli from your bank account to your vendors without setting up or funding a settlement account.

Handle consolidated and partial payments

Get maximum payment flexibility to make partial payments, consolidate payments, or issue vendor credits.

Take control of your ACH vendor payments. Contact Stampli today for a free demo of Stampli Direct Pay.